March 30, 2025

14 min

Published: March 17, 2024

|

Updated: April 28, 2026

There are 20 common types of invoices, grouped into three categories: standard invoices (the everyday request for payment), project-based invoices (for long or milestone-driven work), and credit and memo invoices (for corrections, refunds, and overdue balances).

The right invoice type depends on three things: what you are billing for (a one-off sale, an ongoing retainer, a milestone, a correction), who the customer is (business, consumer, or overseas buyer), and which jurisdiction you sell in. This guide defines all 20 types, shows examples, and summarises the legal requirements in the US, UK, Australia, and the European Union.

# | Invoice type | Category | One-line purpose |

1 | Standard (sales) invoice | Standard | The default request for payment for goods or services delivered |

2 | Proforma invoice | Standard | A preliminary estimate sent before the sale is confirmed |

3 | VAT / tax invoice | Standard | A sales invoice that itemises VAT or GST for tax reporting |

4 | Commercial invoice | Standard | Required for cross-border shipments; used by customs |

5 | Retail invoice | Standard | A simplified invoice issued at the point of sale to consumers |

6 | Purchase invoice | Standard | The same document viewed from the buyer’s side |

7 | Self-billing invoice | Standard | The buyer issues the invoice on behalf of the seller |

8 | Consolidated invoice | Standard | Combines multiple transactions into a single invoice |

9 | E-invoice | Standard | A structured digital invoice exchanged between systems |

10 | Simplified invoice | Standard | A short-form invoice allowed below a national threshold |

11 | Recurring invoice | Project-based | Sent on a fixed schedule for subscriptions or retainers |

12 | Retainer invoice | Project-based | Payment requested in advance to reserve future work |

13 | Interim (progress) invoice | Project-based | Partial payment as a project advances |

14 | Timesheet invoice | Project-based | Billed against logged hours at agreed rates |

15 | Milestone invoice | Project-based | Issued when a pre-agreed project milestone is met |

16 | Final invoice | Project-based | The last invoice closing out a completed project |

17 | Credit note (credit memo) | Credit & memo | A negative invoice that reduces what the customer owes |

18 | Debit note (debit memo) | Credit & memo | An invoice that increases what the customer owes |

19 | Mixed invoice | Credit & memo | Combines credit and debit adjustments into one document |

20 | Past-due (overdue) invoice | Credit & memo | A resent invoice reflecting late fees or interest |

An invoice is a document issued by a seller to request payment from a buyer, and the “type” of invoice defines the specific situation it is used for — a one-off sale, a recurring charge, a milestone, a correction, or an international shipment.

Every invoice contains the same core fields — a unique invoice number, the seller’s and buyer’s details, an itemised list of goods or services, totals, tax, and payment terms — but the purpose and legal status of the document depend on the type. A proforma invoice, for example, contains every field a standard invoice does, yet it is not a legal request for payment. A commercial invoice carries the same fields plus customs-specific data that is legally required for cross-border shipments. For a full breakdown of the fields every invoice must contain, see our guide to the essential invoice elements.

The “type” is defined by three questions:

Choosing the correct type is not cosmetic — it determines whether the document is legally enforceable, whether the buyer can reclaim VAT, and whether tax authorities will accept the invoice as a valid record. Getting it wrong is one of the top audit red flags across the jurisdictions covered below.

Invoices fall into three categories: standard invoices (the default request for payment for a completed sale), project-based invoices (used across long or milestone-driven work), and credit and memo invoices (used to correct, adjust, or chase prior invoices).

Every one of the 20 types below fits into exactly one of these three categories. The category determines the billing cadence (one-off, ongoing, or adjustment), the legal framing (payment request, advance, or correction), and the accounting treatment. The matrix below is the quickest way to locate the type you need.

Category | What it covers | When to use | Types it includes |

Standard | The everyday request for payment for goods or services delivered | One-off sales, point-of-sale transactions, cross-border shipments | Standard, proforma, VAT/tax, commercial, retail, purchase, self-billing, consolidated, e-invoice, simplified (10 types) |

Project-based | Billing across long or milestone-driven engagements | Retainers, subscriptions, construction, consulting, agency work | Recurring, retainer, interim, timesheet, milestone, final (6 types) |

Credit & memo | Corrections, refunds, adjustments, and follow-ups on prior invoices | Returns, billing errors, additional charges, overdue collection | Credit note, debit note, mixed, past-due (4 types) |

Standard invoices dominate small-business billing, but the remaining 19 types are what separate a compliant business from one that runs into payment delays and audit findings. The rest of this guide defines each type, gives an example, and explains when to use it.

Standard invoices are the 10 most common documents businesses use to request payment for a completed or imminent sale, ranging from the everyday sales invoice to jurisdiction-specific variants like the VAT invoice and commercial invoice.

Every business will issue at least one type from this group. Most small businesses use only 2–3 of them day-to-day, with the remainder reserved for specific scenarios like cross-border shipments, buyer-generated billing, or transactions below a simplified-invoice threshold.

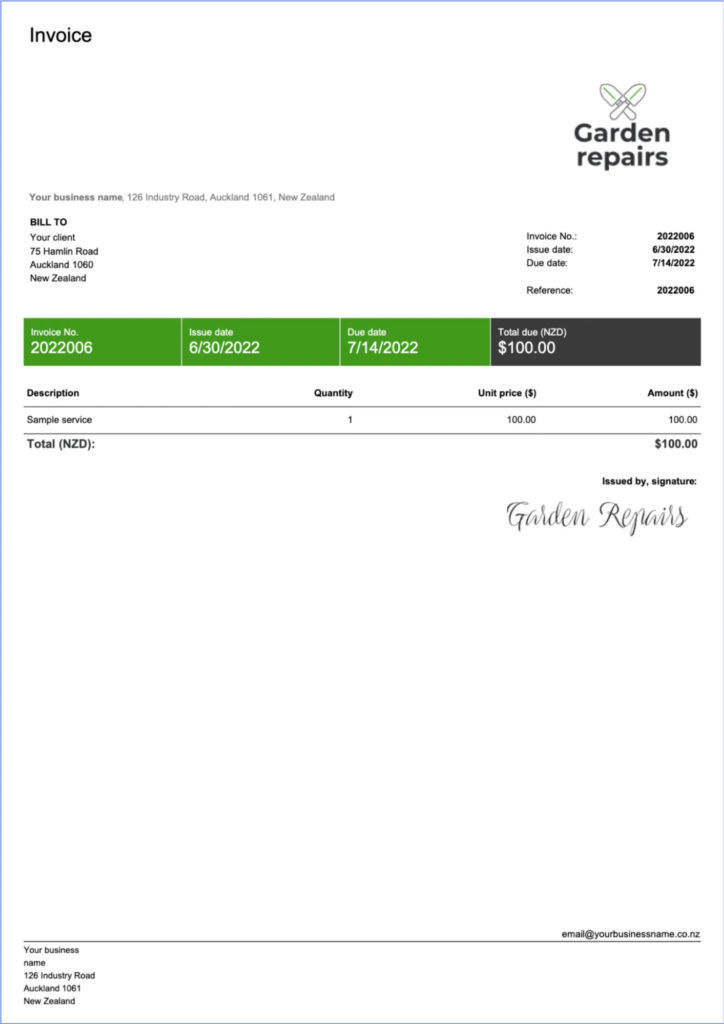

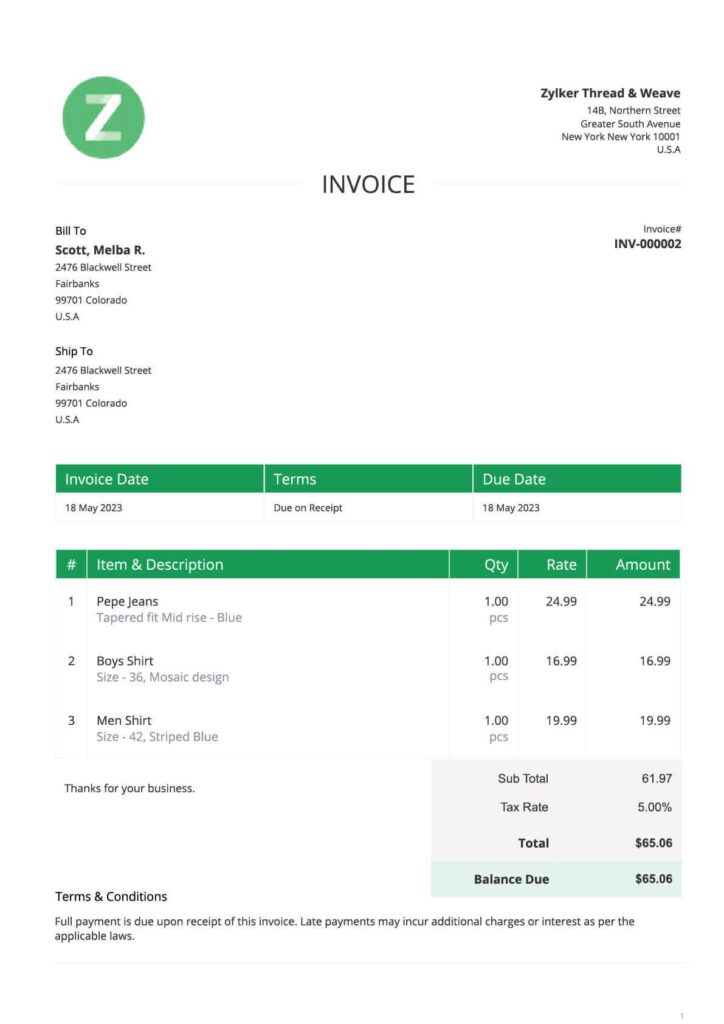

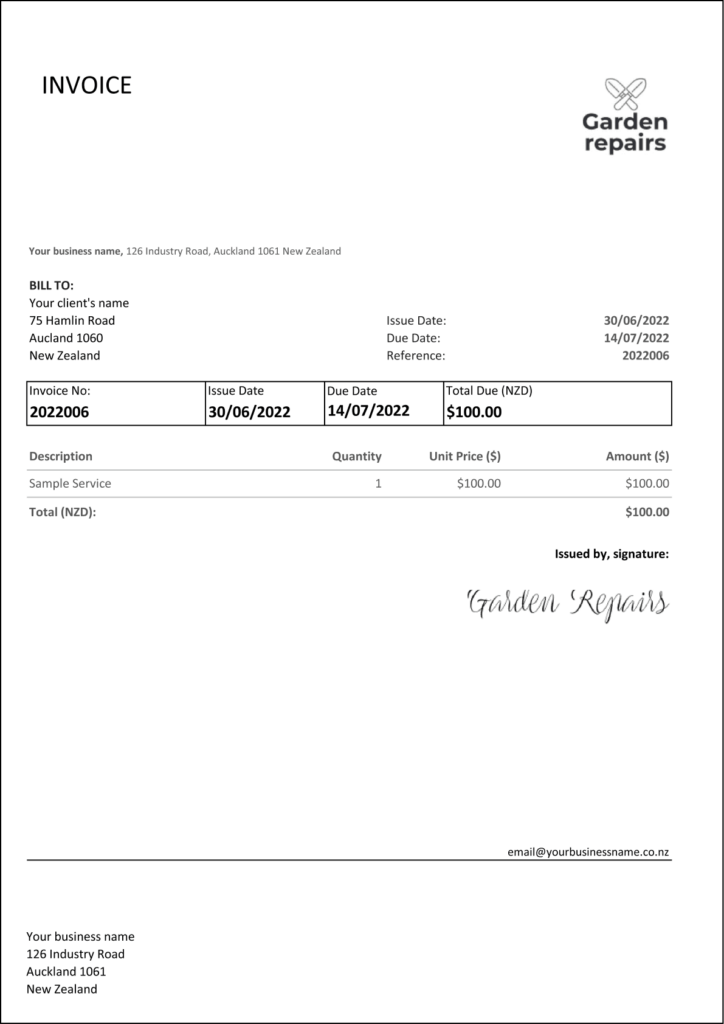

The standard sales invoice is the default request for payment a seller sends after delivering goods or services. It is also called a regular invoice or basic invoice. It is the document most people picture when they hear the word “invoice”.

Every standard invoice must contain a unique invoice number, the seller and buyer details, an itemised list with quantities and prices, tax, total, payment terms, and the issue date. For a full breakdown of required fields, see our guide on what does a professional invoice template look like.

Example: A graphic designer completes a logo project and sends an invoice for $1,200 with 14-day payment terms.

Best for: Any business issuing one-off sales of goods or services.

(Source: Billdu Invoice Template)

(Source: Billdu Invoice Template)

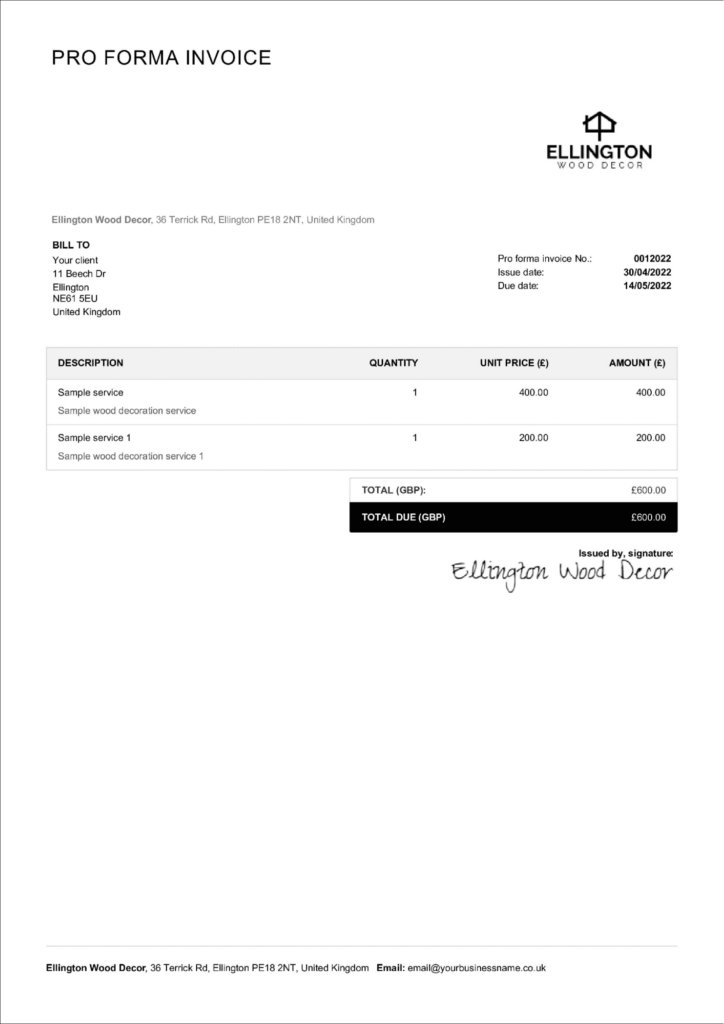

A proforma invoice is a preliminary document sent before a sale is finalised, setting out the expected goods, quantities, and price. It is not a legal request for payment — no accounting entry is made against it, and the buyer is not obliged to pay from it alone.

Proforma invoices are often confused with quotes or estimates. The difference is mostly formal: a proforma invoice is laid out to look exactly like the final invoice, whereas a quote is freer in format. For the full comparison, see our quote vs invoice guide.

Example: A small manufacturer sends a proforma invoice for 500 units at $8 each — $4,000 plus shipping — so the buyer can approve the order and arrange payment.

Best for: Deal negotiation; international trade where advance approval is needed before shipping.

(Source: Billdu Proforma Invoice Template)

3. VAT / tax invoice

A VAT invoice — called a tax invoice in Australia and some other jurisdictions — is a standard invoice that itemises VAT or GST separately so the buyer can reclaim it and the tax authority can verify the seller’s reporting. It is a legal document; the rules governing its format are set by each country’s tax authority.

In the UK and across the EU, VAT invoices must contain a unique sequential invoice number, the seller’s VAT registration number, and the VAT rate and amount for each line. See the legal requirements by country section below for the specifics in each jurisdiction.

Example: A UK consultancy bills £2,000 net, adds £400 VAT at 20%, and shows both amounts separately on the invoice with the VAT registration number.

Best for: Any VAT- or GST-registered business; B2B transactions where the buyer needs to reclaim tax.

(Source: Zervant Tax Invoice Template)

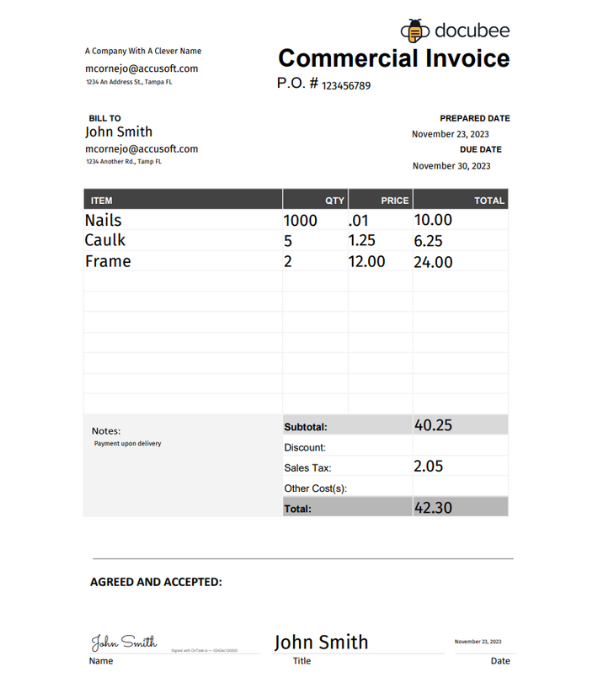

A commercial invoice is a legally required document for cross-border shipments of goods. Customs authorities use it to calculate duties and taxes and to clear the shipment. It contains the standard invoice fields plus additional data specific to customs: country of origin, Harmonised System (HS) code, weight, and shipping terms (usually an Incoterms reference).

A commercial invoice is not issued for purely domestic sales. It is only required when goods cross an international border.

Example: A UK-based clothing exporter ships £10,000 of apparel to a buyer in the US and issues a commercial invoice showing the HS code, country of origin (UK), and Incoterms DAP for customs clearance.

Best for: Importers, exporters, and any small business selling physical goods to overseas buyers.

(Source: Docubee Commercial Invoice Template)

A retail invoice is a simplified document issued to consumers at the point of sale. It confirms the transaction, details what was purchased, and serves as a receipt. In most jurisdictions, retail invoices are exempt from some of the stricter formatting requirements that apply to B2B invoices, on the assumption that the buyer is not reclaiming tax.

Retail invoices are sometimes called retail receipts. In many jurisdictions, a simple retail receipt is acceptable below a certain threshold; above it, a full invoice is required. See how to write a receipt for the receipt-specific conventions.

Example: A brick-and-mortar shop issues a printed retail invoice at the till for a $120 clothing purchase, listing the items and total sales tax.

Best for: B2C retail — stores, restaurants, cafés, salons, and e-commerce consumer sales.

(Source: Zoho Retail Invoice Template)

A purchase invoice is the same document as a standard invoice viewed from the buyer’s side. When a supplier issues a sales invoice, the buyer records it in their accounts payable ledger as a purchase invoice. It is also called a vendor invoice or a bill.

Purchase invoices are commonly confused with purchase orders. They are different documents. A purchase order is issued by the buyer before the sale to authorise it; a purchase invoice is the sales invoice received from the supplier after delivery. See our full guide on purchase order vs invoice for the comparison.

Example: A café receives an invoice for $800 of coffee beans from its wholesaler. The wholesaler calls it a sales invoice; the café records it as a purchase invoice.

Best for: Any business tracking expenses and reconciling supplier payments.

A self-billing invoice is issued by the buyer on behalf of the seller. Both parties must formally agree to the arrangement in advance, and the seller must accept the invoices as equivalent to their own. It is common in industries where the buyer has better data on quantities or rates than the seller — for example, a publisher paying royalties to an author, or a supermarket paying a produce supplier by weight received.

Self-billing is specifically regulated in the UK (HMRC VAT Notice 700/62) and in the EU VAT Directive. Both require a written self-billing agreement between the parties.

Example: A publisher issues a self-billing invoice each quarter to an author, calculating royalty amounts from internal sales data, and sends the invoice to the author for their records.

Best for: Royalty payments, agricultural supply, and high-volume procurement where the buyer holds the measurement data.

A consolidated invoice combines multiple individual transactions with the same buyer into a single document, typically issued at the end of a billing period. It replaces sending a separate invoice for each transaction, which reduces administrative overhead on both sides.

Consolidated invoices are common in B2B supply relationships where many small deliveries are made to the same buyer. In the EU, the VAT Directive explicitly permits consolidated invoices as long as each underlying transaction is identifiable within the document.

Example: A wholesale food distributor makes 18 deliveries to a restaurant group in March and issues one consolidated invoice at month-end for all 18 orders, itemised by date.

Best for: Wholesalers, logistics providers, and any supplier delivering frequently to the same buyer.

An e-invoice is a structured digital invoice exchanged directly between the seller’s and buyer’s systems in a machine-readable format (typically XML or a Peppol-compliant format). An e-invoice is not the same as a PDF invoice emailed as an attachment — a PDF is a digital version of a paper invoice; an e-invoice is structured data.

E-invoicing is becoming legally mandated across the EU. Italy has required B2B e-invoicing since 2019. Germany’s mandate phased in from 2025. France’s mandate begins in 2026. Spain and Poland have active rollouts. Businesses selling into the EU should confirm the current status in each destination country.

Example: A French supplier sends an e-invoice via the Peppol network to a German buyer. Both systems parse the XML, post the entry automatically, and reconcile the VAT.

Best for: Any business selling into jurisdictions with active e-invoicing mandates; B2B supply chains at scale.

A simplified invoice is a short-form invoice permitted below a national value threshold, most commonly in the UK and across the EU. It requires fewer data fields than a full invoice — for example, the buyer’s details may be omitted. Simplified invoices cannot be used to reclaim VAT in B2B settings, which is why most businesses still issue full invoices for their B2B sales.

Thresholds vary by country. The UK allows simplified VAT invoices below £250 (including VAT). Germany’s threshold is €250. Spain’s is €400. A B2B customer who needs to reclaim VAT can always request a full invoice instead.

Example: A UK café issues a simplified VAT invoice for a £15 lunch purchase showing only the business name, date, total, and VAT rate — no customer details.

Best for: Low-value B2C transactions in jurisdictions with a simplified-invoice threshold.

Project-based invoices are six billing documents used for long or milestone-driven work, ranging from recurring retainers to final-project close-outs.

Project-based types are designed around one reality: the work and the payment happen on different timelines. Recurring invoices keep cash flow predictable for subscription work. Interim and milestone invoices break large projects into manageable payments. Final invoices close out the engagement. Retainer and timesheet invoices handle two common freelance and agency billing models. Used correctly, they compress the gap between delivering work and getting paid — the single biggest driver of small-business cash flow health.

A recurring invoice is issued on a fixed schedule — weekly, monthly, quarterly, or annually — for the same goods or services at the same price. It is the standard billing document for subscription businesses, SaaS platforms, retainer clients, and any ongoing supply arrangement.

Recurring invoices are typically automated. An invoicing platform generates the invoice on the scheduled date, emails it to the customer, and in some setups charges a stored payment method. Automation with recurring invoice automation eliminates the admin overhead and the risk of skipping a billing cycle.

Example: A SaaS company issues a recurring invoice for £49 on the 1st of every month to each of its annual subscribers, automatically charging the card on file.

Best for: SaaS, subscriptions, consulting retainers, managed services, and any ongoing service.

(Source: Inv24 Recurring Invoice Template)

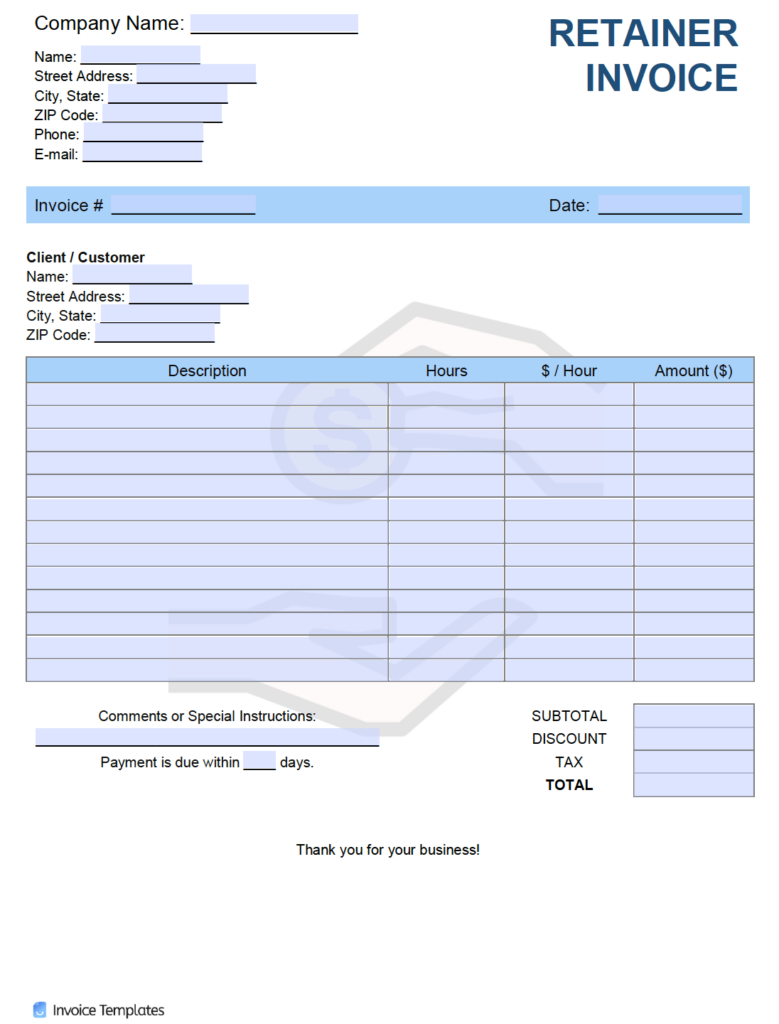

A retainer invoice requests payment in advance for work that will be delivered in the future. The buyer pays to reserve the seller’s capacity — time, expertise, or production slots — typically over a defined period. Retainer invoices are common among lawyers, consultants, and agencies where the value is in availability as much as in the deliverable itself.

A retainer is not the same as a deposit. A deposit is a partial payment against a specific project; a retainer is a fixed payment for access to future services within a period. The two are sometimes confused and are worth keeping distinct in contracts.

Example: A marketing consultant issues a monthly retainer invoice for $2,500, covering 20 hours of work the client can draw on through the month.

Best for: Lawyers, consultants, marketing and PR agencies, and any business selling capacity or availability.

(Source: InvoiceGenerator Retainer Invoice Template)

An interim invoice — also called a progress invoice — requests partial payment while a long project is still in progress. It is typically issued at set points: every two weeks, monthly, or at an agreed percentage of completion. Interim invoicing keeps cash flow steady during projects that would otherwise leave the seller unpaid for months.

Interim invoicing is common in construction, engineering, software development, and any project billed above a few thousand dollars. Partial payments on invoices should be agreed in the contract up front — the schedule, the amounts, and the conditions for release.

Example: A builder on a six-month kitchen renovation invoices $8,000 at the end of month 1 (demolition complete), $12,000 at month 3 (cabinetry installed), and the balance on the final invoice.

Best for: Construction, engineering, software development, agencies, and any project billed above $5,000.

A timesheet invoice is calculated from logged hours multiplied by an agreed hourly rate, rather than from fixed line items. It is the standard billing document for freelancers, contractors, and consultants who charge by the hour. Each line on the invoice typically shows the date, task, hours, and rate.

Accurate time tracking is the foundation of a timesheet invoice. Most invoicing platforms integrate with time trackers so logged hours flow directly into the invoice, avoiding the reconciliation work of matching timesheets to invoice lines manually.

Example: A freelance developer logs 32 hours in June across three tasks, at $85 per hour, and issues a timesheet invoice for $2,720 with the task breakdown.

Best for: Freelancers, contractors, consultants, and any hourly-billed service work.

(Source: Billdu Time-Sheet Invoice Template)

A milestone invoice is issued when a pre-agreed project milestone is completed — for example, delivery of a design brief, completion of a software feature, or sign-off on a prototype. It differs from an interim invoice in that the trigger is a specific deliverable, not the passage of time.

Milestone invoicing is strongest when milestones are clearly defined in the contract. Vague milestones (“first draft”) lead to payment disputes; specific milestones (“signed-off design specification document delivered”) do not.

Example: A design agency invoices $5,000 when the client signs off on the brand strategy, $7,000 on final brand guidelines, and the balance on delivery of the website.

Best for: Agencies, design firms, software projects, and any deliverable-based engagement.

A final invoice is the closing invoice at the end of a project. It consolidates the total contracted value, deducts all prior interim, milestone, and retainer payments, and requests the remaining balance. It serves as the project’s formal close-out document — the trigger for final sign-off and any retention release.

A final invoice typically references the prior invoice numbers it follows from, so the buyer’s accounts-payable team can reconcile it against earlier payments in one place.

Example: A contractor completes a $60,000 renovation. Prior interim invoices have collected $48,000. The final invoice requests the remaining $12,000 and references all three prior invoice numbers.

Best for: Any project with interim billing; construction, consulting, and agency work.

(Source: Billdu Blank Invoice Template)

Credit and memo invoices are four documents used to correct, adjust, or follow up on prior invoices, including credit notes, debit notes, mixed invoices, and past-due invoices.

Credit and memo invoices preserve the integrity of an accounting sequence by never amending or deleting an original invoice. Instead, they issue a companion document that references the original and adjusts the balance. This is how HMRC, the ATO, the IRS, and the EU VAT Directive expect corrections to be handled — and a frequent audit red flag when businesses delete or overwrite invoices instead.

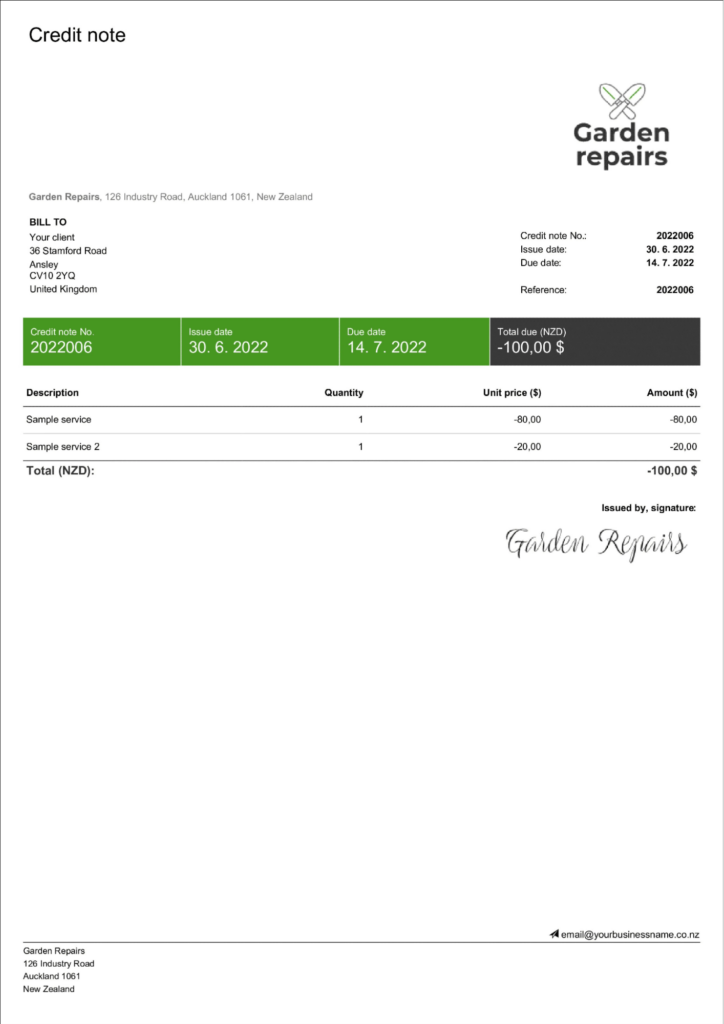

A credit note is a negative invoice issued to reduce what the buyer owes, typically as a refund, return, or correction to an earlier invoice. Every credit note must reference the original invoice it adjusts and must carry its own unique identifier from a separate numbering sequence (not the sales-invoice sequence).

A credit note is the correct way to correct an over-billing — never by amending or deleting the original invoice. Use a credit note for refunds, short deliveries, damaged goods, and any reduction in the amount owed.

Example: A furniture supplier invoices $2,000 for 10 chairs. One arrives damaged. The supplier issues a credit note for $200 referencing invoice INV-2026-0142, reducing the buyer’s balance to $1,800.

Best for: Refunds, returns, billing errors, short deliveries, and post-sale adjustments.

(Source: Billdu Credit Invoice Template)

A debit note is the opposite of a credit note — an invoice that increases the amount the buyer owes. It is used for additional charges that apply after the original invoice was issued, such as tax corrections, additional work agreed after the fact, or handling fees that were previously missed.

Debit notes must also reference the original invoice and use their own numbering sequence. They are legally distinct documents, not modifications of the original invoice.

Example: A consultancy under-bills a client by $400 due to a rate correction. A debit note for $400 is issued referencing the original invoice, bringing the total owed to its corrected amount.

Best for: Post-invoice rate corrections, additional agreed work, and missed charges.

A mixed invoice combines credit and debit adjustments into a single document, presenting the net effect to the buyer. It is useful when multiple adjustments apply to the same billing cycle — for example, credit for service downtime offset by additional charges for added users.

Mixed invoices can net to a positive, negative, or zero balance. They are relatively uncommon because most businesses prefer to issue credit and debit notes separately for clarity, but they are legal and accepted in most jurisdictions.

Example: A SaaS provider issues a mixed invoice with a $200 credit for downtime and a $320 debit for additional user licences added mid-month. Net: $120 owed by the buyer.

Best for: Billing cycles with both credits and additional charges; SaaS, utilities, telecommunications.

A past-due invoice is a re-sent invoice issued after the original payment due date has passed, typically incorporating late fees or interest per the original payment terms. It is not a new sale — it is a collection document reminding the buyer of an unpaid invoice, with the updated balance.

Past-due invoices work best when the late-fee terms were set in the original invoice. Without pre-agreed terms, adding late fees after the fact is hard to enforce. Automating the reminder process with automatic payment reminders reduces the admin burden and typically brings payments in faster than manual chasing.

Example: An invoice for $1,500 with 30-day terms and a 1.5% monthly late fee is unpaid at day 45. A past-due invoice is issued for $1,522.50, referencing the original invoice number.

Best for: Any business collecting on overdue accounts.

Discover the versatility in invoicing – create different types with Billdu!

Free 7-day trialNo credit card requiredCancel anytime

Free 7-day trialNo credit card requiredCancel anytime

To choose the right invoice type, match the scenario — one-off sale, recurring service, project milestone, cross-border shipment, or correction — to one of the 20 types using the decision table below.

The right invoice type is almost always obvious once the scenario is named. The table below maps common small-business situations to the invoice type that applies. If the situation spans more than one row — for example, a cross-border recurring service — issue the more specific type; commercial invoices take priority over recurring for international shipments.

Scenario | Invoice type | Why |

One-off sale of goods or services | Standard invoice | Default for any domestic sale |

Before the sale is confirmed | Proforma invoice | Sets the terms; buyer not yet obliged to pay |

VAT or GST is applicable | VAT / tax invoice | Required for the buyer to reclaim tax |

Goods crossing an international border | Commercial invoice | Required by customs |

Retail or consumer transaction | Retail invoice or simplified invoice | Shorter-form, no VAT reclaim needed |

Below national simplified-invoice threshold | Simplified invoice | Fewer fields required |

Selling into EU with e-invoicing mandate | E-invoice | Legally mandated in Italy, Germany, France, others |

Subscription or retainer service | Recurring invoice | Fixed schedule, same amount |

Advance payment for future work | Retainer invoice | Reserves capacity |

Partial payment during long project | Interim invoice | Keeps cash flow steady |

Triggered by deliverable completion | Milestone invoice | Specific event rather than schedule |

Billing by logged hours | Timesheet invoice | Variable amount, based on time worked |

Closing out a completed project | Final invoice | Reconciles against prior interim invoices |

Refund, return, or over-billing correction | Credit note | Reduces amount owed; references original |

Additional charges after original invoice | Debit note | Increases amount owed; references original |

Multiple credit and debit adjustments | Mixed invoice | Nets to a single balance |

Overdue invoice with late fees | Past-due invoice | Collection document, not a new sale |

High volume of small transactions, same buyer | Consolidated invoice | Reduces admin overhead |

Buyer has the measurement data | Self-billing invoice | Buyer issues on seller’s behalf by agreement |

Once the correct invoice type is identified, the mechanics of producing it are the same: add a unique invoice number, itemise the line items, apply the correct tax, and follow through with invoice tracking best practices to reconcile payments against the invoice. For a step-by-step walkthrough of the invoicing process end to end, see how to make an invoice. You can also create a professional invoice for free with Billdu’s free invoice generator — it defaults to a standard sales invoice and lets you switch to proforma, recurring, or credit-note formats without changing tools.

Legal requirements for invoice types vary by country: the UK and EU mandate VAT invoices for VAT-registered businesses, Australia requires specific Tax Invoice wording, and EU member states are phasing in B2B e-invoicing mandates between 2024 and 2028.

The rules below summarise the invoice-type requirements in four jurisdictions that cover most small-business sellers globally. Always verify current rules with the relevant tax authority before making changes — these requirements are updated regularly, particularly around e-invoicing mandates.

The IRS does not mandate specific invoice types but requires adequate records for all income, meaning every sale must be supported by an invoice carrying a unique identifier and full transaction details.

US federal law does not prescribe which invoice type to use. The IRS’s requirement, set out in Publication 334 (Tax Guide for Small Business) and Publication 583 (Starting a Business and Keeping Records), is that a business maintain “permanent, accurate, and complete records” of all income and deductions. A standard sales invoice satisfies this requirement for most B2B and B2C transactions.

US businesses selling internationally must issue commercial invoices for all exported goods. US sales tax is levied at the state level, not federally, so sales-tax reporting requirements vary by state.

Primary sources: IRS Publication 334 — Tax Guide for Small Business; IRS Publication 583 — Starting a Business and Keeping Records.

HMRC requires VAT-registered UK businesses to issue VAT invoices within 30 days of supply, with a unique sequential invoice number, the seller’s VAT registration number, and VAT itemised separately.

VAT invoices in the UK must follow the format set out in HMRC VAT Notice 700/21. Simplified invoices are permitted below £250 including VAT. Self-billing invoices require a written agreement between the parties per HMRC VAT Notice 700/62. Credit notes must use a separate numbering sequence from sales invoices.

Non-VAT-registered UK businesses are not required to issue VAT invoices but must still keep records sufficient for HMRC under the standard record-keeping rules. VAT records, including invoices, must be kept for at least 6 years.

Primary sources: GOV.UK — Invoicing and taking payment from customers; HMRC VAT Notice 700/21 (Keeping VAT records); HMRC VAT Notice 700/62 (Self-billing).

The Australian Taxation Office requires GST-registered businesses to issue a tax invoice within 28 days of a customer request for any taxable sale of AUD 82.50 or more, prominently labelled “Tax invoice”.

Australian tax invoices are governed by GSTR 2013/1. The invoice must include the words “Tax invoice”, the seller’s ABN, the GST amount, and for sales of AUD 1,000 or more the buyer’s identity or ABN. Standard sales invoices below AUD 82.50 do not have to be issued as tax invoices.

Australia has adopted the Peppol framework for B2B e-invoicing. Peppol e-invoicing is not yet mandatory but is actively encouraged by the ATO. Tax invoices must be kept for at least 5 years.

Primary sources: ATO — Tax invoices; GSTR 2013/1 (Goods and services tax: tax invoices); business.gov.au — How to invoice.

The EU VAT Directive requires every invoice issued in a member state to carry a sequential number and standard data fields, with B2B e-invoicing mandates phasing in across member states between 2024 and 2028.

Council Directive 2006/112/EC sets out the baseline rules for invoices across all EU member states — sequential numbering, VAT itemisation, seller and buyer identification. Individual member states may add requirements; Germany’s GoBD rules, for example, require tamper-proof invoice systems. Simplified invoices are permitted below national thresholds (typically €250–€400 depending on the country).

The biggest change underway is the Europe-wide move to mandatory B2B e-invoicing. Italy has required it since 2019. Germany’s phased rollout began in January 2025. France’s B2B e-invoicing mandate begins in 2026. Spain and Poland have active rollouts in 2025–2026. Any small business selling B2B into these countries must issue e-invoices in the mandated format.

Primary source: Council Directive 2006/112/EC on the common system of value added tax (the EU VAT Directive); national tax-authority websites for member-state-specific rules.

The six most common mistakes small businesses make when choosing an invoice type are sending a proforma instead of a standard invoice, missing the “Tax invoice” label in Australia, deleting instead of crediting, mixing credit-note numbering with sales, skipping commercial invoices on exports, and using PDF invoices where e-invoicing is mandated.

Each of these mistakes is either a legal-compliance issue or a payment-delay issue. Every one is easy to avoid once it has been flagged.

This guide is based on primary tax-authority documentation from the IRS, HMRC, ATO, and the EU VAT Directive, cross-checked against the official guidance and conventions in use across the leading invoicing platforms as of Q1 2026.

All legal requirements were verified against primary government sources in April 2026. Invoice-type definitions reflect the conventions in use across the leading invoicing platforms as of Q1 2026, cross-checked against the official tax-authority guidance in each of the four jurisdictions covered. Every legal claim links to a primary source; every statistic is dated.

Primary sources consulted:

Experience a seamless invoicing process with Billdu like never before. Try it for free today!

Free 7-day trialNo credit card requiredCancel anytime

Sign up now for a 30-day free trial and get 20% off on your first subscription

By signing up you agree to Terms of use and Privacy policy