March 30, 2025

12 min

Published: October 7, 2024

|

Updated: April 29, 2026

An invoice is a document a seller sends a buyer to request payment for goods or services. A receipt is a document a seller issues after payment is received, confirming the transaction is complete.

The key difference is timing and purpose: invoices request payment before money changes hands, while receipts confirm payment after it has been made. Both documents are legally required in most countries for business-to-business transactions, and both are essential for tax compliance, audit readiness, and clean bookkeeping.

Feature Invoice Receipt Purpose The seller This specific invoice document Issued The buyer The buyer’s internal purchase authorisation Contains The seller The payment transaction itself Legal role The seller The client relationship, not the transaction Used for Tracking accounts receivable Tax deductions, returns, warranty claims Numbering Sequential and legally required in UK/EU Unique but flexibility allowed Common example Freelancer billing for a finished project Cashier slip after a cash purchase

An invoice is a formal document a seller issues to a buyer to request payment for goods delivered or services rendered, listing the items sold, amount owed, and payment due date.

Most businesses issue invoices after work is completed but before payment is received. An invoice creates a record of the transaction for both parties and serves as a legally binding request for payment under agreed terms. In accounting, each unpaid invoice sits in accounts receivable until the buyer pays — which is why tracking them carefully matters for cash flow.

Every invoice should contain the following elements. For a deeper walkthrough of each field, see our guide to the essential invoice elements:

A receipt is a document a seller issues to a buyer after payment has been received, confirming that the transaction is complete and serving as proof of purchase.

Receipts are used for bookkeeping, tax reporting, product returns, and warranty claims. Unlike invoices, receipts are almost always issued at or immediately after the moment of payment — whether in a retail shop, after an online checkout, or once a client pays a freelancer’s invoice.

Most receipts contain the following elements:

Receipts come in several common formats, each suited to different payment situations. The receipt format varies by transaction type, but the core elements above remain the same.

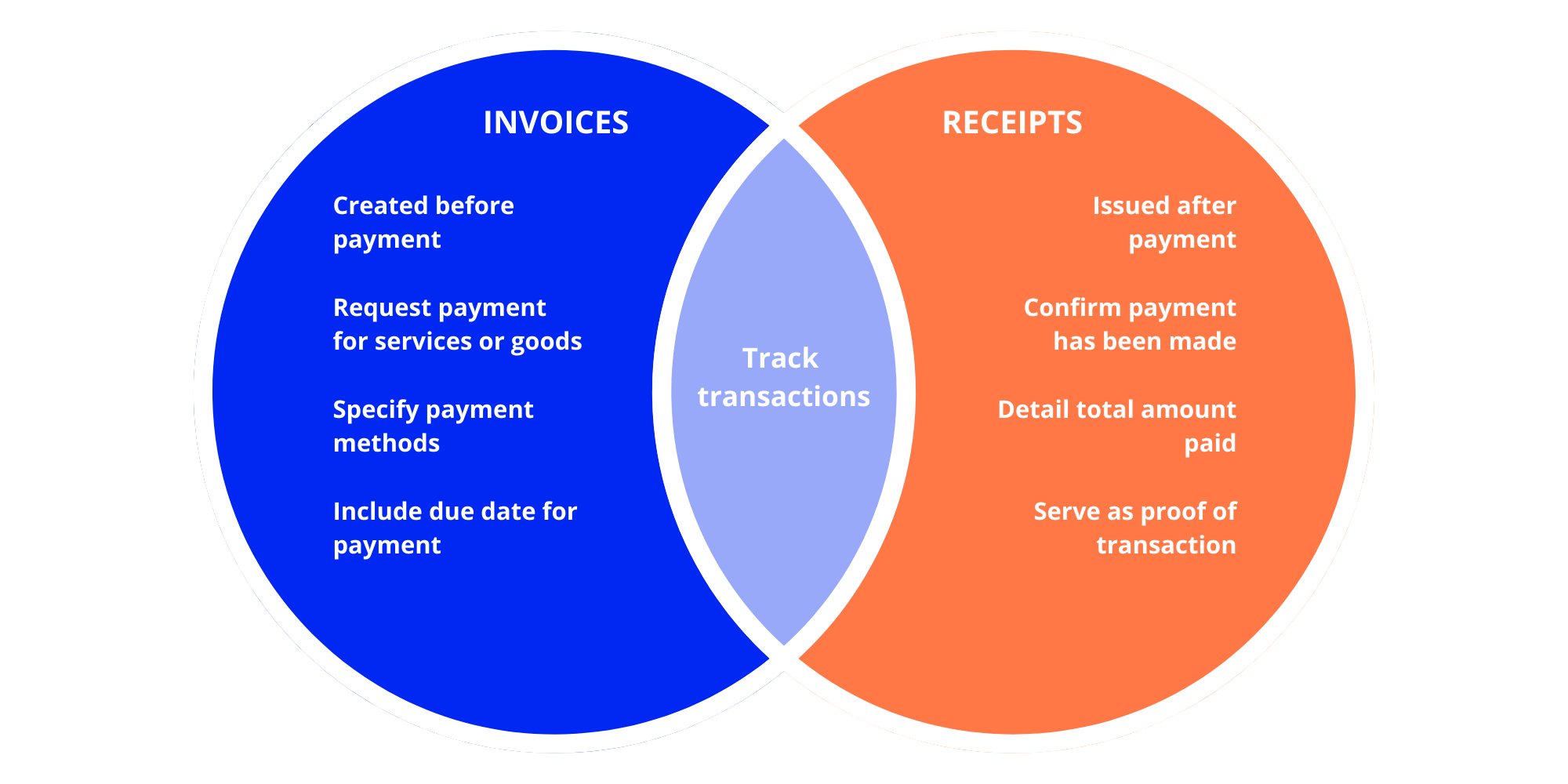

Invoices and receipts document different stages of the same transaction. Here are the seven differences that matter most for small businesses.

Invoices are issued before payment; receipts are issued after payment.

An invoice is sent when work is complete or goods are delivered but before the buyer has paid. A receipt is issued the moment payment is received. The timing difference is the single clearest way to tell which document is which.

Invoices request payment; receipts confirm payment.

An invoice exists to tell a buyer how much they owe and when to pay. A receipt exists to document that the buyer has paid. Using one in place of the other creates confusion and legal risk — an invoice alone is not proof that money changed hands.

Invoices contain more detail than receipts.

An invoice lists every line item, quantity, unit price, tax rate, payment terms, and due date. A receipt typically shows only the total paid, the date, and the method of payment. This is because invoices must enable dispute resolution; receipts just need to confirm a completed transaction.

An invoice is evidence of a sale agreement; a receipt is proof of payment.

An invoice becomes legally binding when accepted by the buyer. A receipt is legally useful as proof that money changed hands — important for tax deductions, returns, and warranty claims.

Invoices belong in accounts receivable; receipts confirm income.

When you issue an invoice, the amount is recorded as accounts receivable — money owed to you. When the invoice is paid and you issue a receipt, the amount moves from accounts receivable into realised revenue. Any partial payments trigger a partial receipt rather than a full one, and the remaining balance stays in accounts receivable.

Invoices are most common in service businesses and B2B sales; receipts are standard in retail and point-of-sale transactions.

A freelance designer almost always issues invoices. A coffee shop almost always issues receipts. Businesses that do both (e.g., a tradesperson billing for a large job but also selling materials on the spot) issue both documents routinely.

Invoices require sequential numbering by law in most countries; receipts have more flexible numbering rules.

Tax authorities including HMRC in the UK and the ATO in Australia require invoices to be numbered in a continuous, gap-free sequence. Receipts must be uniquely identifiable but do not always require strict sequencing. Retention periods differ too — see the legal-requirements section below for the full breakdown. Avoiding common invoicing mistakes in this area is the easiest way to stay audit-ready.

Whether you need to issue an invoice, a receipt, or both depends on the transaction type. Here are four common scenarios.

Freelancers issue an invoice when a project is finished, then issue a receipt once the client pays.

A graphic designer finishes a logo and emails the client an invoice for $1,500 with Net 30 payment terms. Three weeks later the client pays by bank transfer. The designer then issues a receipt confirming the $1,500 payment and the date it was received. Both documents are now part of the project’s paper trail for tax purposes.

Retail shops issue a receipt immediately at the point of sale; no invoice is needed.

A customer buys a pair of shoes for $80 and pays with a card. The shop prints a receipt right away. No invoice is issued because payment and delivery happen simultaneously. The receipt alone documents the full transaction.

Subscription businesses issue a receipt after each successful recurring payment.

A SaaS company charges $49/month to a customer’s card on the first of each month. Each month, the customer receives an email receipt confirming the charge. Most recurring invoices platforms handle this automatically — the invoice, payment, and receipt are generated as a single chain.

B2B wholesale transactions typically involve an invoice before delivery and a receipt after payment clears.

A restaurant orders $4,000 worth of supplies from a wholesaler with Net 30 terms. The wholesaler ships the goods with a delivery note and issues an invoice dated the day of shipment. The restaurant pays via bank transfer within the 30-day window; the wholesaler then issues a receipt documenting the payment date and method.

Create invoices and receipts easily with the Billdu app. Download now and streamline your business transactions!

Free 7-day trialNo credit card requiredCancel anytime

Free 7-day trialNo credit card requiredCancel anytime

An invoice can serve as a receipt only when it is clearly marked “Paid” and shows the date and method of payment; otherwise it remains a request for payment, not proof of one.

Most invoicing software handles this automatically: when you mark an invoice as paid, the document is reissued with “Paid” stamped across it and the payment details appended. In Australia, the ATO accepts a marked-paid invoice as a valid tax invoice and receipt for most purposes. In the UK, HMRC expects the same so long as all VAT-invoice requirements are met.

In practice, using a combined document is fine for small cash or card sales. For any substantial transaction, best practice is to issue a separate invoice and receipt. This keeps your bookkeeping clean, your audit trail clear, and your client’s accounts-payable system happy.

Invoice and receipt requirements are set by each country’s tax authority and vary by VAT, GST, and sales-tax rules.

Below is a summary for four major markets. Always check the original government source for the latest rules — these change periodically.

The IRS treats invoices and receipts as supporting documents that must substantiate the income and deductions reported on a business’s tax return.

US federal law does not prescribe a specific invoice numbering system. What the IRS does require, through Publication 583, is that businesses keep “permanent, accurate, and complete records” sufficient to verify reported income and claimed deductions. Detailed expense tracking is part of this — every deductible expense needs a supporting receipt.

Key points for US small businesses:

Primary source: IRS Publication 583 — Starting a Business and Keeping Records.

HMRC requires VAT-registered UK businesses to issue invoices with a unique, sequential identification number with no gaps in the sequence.

If a UK business is VAT-registered, its invoices must meet a specific format set out in VAT Notice 700/21. HMRC inspectors look at this first during a VAT inspection; unexplained gaps in the sequence can trigger further scrutiny.

Key points for UK small businesses:

Primary sources: GOV.UK — Invoicing and taking payment from customers; HMRC VAT Notice 700/21.

The Australian Taxation Office requires GST-registered businesses to issue a tax invoice within 28 days of a customer request for any taxable sale over AUD 82.50 (including GST).

A valid tax invoice must clearly show the words “Tax invoice” and include the seller’s ABN. Rules are set out in GSTR 2013/1.

Key points for Australian small businesses:

Primary sources: ATO — Tax invoices; GSTR 2013/1; business.gov.au — How to invoice.

Under the EU VAT Directive, every tax invoice issued in a member state must carry a sequential number that uniquely identifies the document, based on one or more series.

Article 226 of Council Directive 2006/112/EC lays out the minimum invoice requirements that apply across all 27 EU member states. Individual countries add requirements on top — Germany’s GoBD rules require a tamper-proof numbering system, France’s Anti-Fraud Law of 2018 mandates certified invoicing software, and Italy requires B2B e-invoicing through the SdI platform.

Key points for EU small businesses:

Primary source: Council Directive 2006/112/EC on the common system of value added tax.

Small businesses can create invoices and receipts using free templates, spreadsheets, or invoicing software — the right choice depends on how many documents you issue each month and whether you need automation.

Method Best for Limitations Free templates (Word, Excel, PDF) Businesses sending fewer than 10 invoices a month Manual numbering, no reminders, no online payment Spreadsheets Freelancers tracking a handful of clients Error-prone, no audit trail, limited scaling Invoicing software Businesses billing regularly or accepting online payments Monthly subscription cost

Invoicing apps automate invoice numbering, track payment status, send automatic payment reminders, and generate receipts the moment a payment is received — removing the most common sources of bookkeeping errors. They also compound: consistent invoicing discipline is the single biggest lever on your cash flow.

💬 Billdu’s take

“The most common mistake we see from small-business owners is treating an invoice and a receipt as interchangeable. They’re not — they document different legal events. An invoice is a claim; a receipt is evidence the claim has been settled. Issuing both, even for small transactions, is the single easiest way to make a future audit painless.”

— David Fačko, SEO Specialist at Billdu

If you send more than a handful of invoices each month, a dedicated tool pays for itself quickly. For a full walkthrough of the end-to-end process, see our guide on how to make an invoice. If you prefer a simple starting point, Billdu’s free invoice generator creates a professional invoice in under 60 seconds, with a valid invoice number and all required elements included automatically. For receipt workflows, our receipt template library covers the most common formats.

This guide is based on primary tax-authority documentation from the IRS, HMRC, ATO, and the EU VAT Directive, cross-referenced with Billdu’s platform experience serving small businesses in 80+ countries since 2012.

All legal requirements were verified against primary government sources in April 2026. Every statistic is dated; every legal claim links to a primary source.

Primary sources consulted:

Run your business from anywhere on Earth or space.

Free 7-day trialNo credit card requiredCancel anytime

Sign up now for a 30-day free trial and get 20% off on your first subscription

By signing up you agree to Terms of use and Privacy policy